Table of Contents

Across both sides of the Atlantic, a recession isn't the primary scenario we're expecting, yet we can all concur that it's not a particularly compelling prediction. A significant factor will likely hinge on the potential reduction of tariffs in China over the coming weeks and, even more importantly, the extent of such reductions.

The media has been highlighting a potential decrease in these rates to 50%–60% from the currently staggering 145%, yet this may not lead to a substantial change in the overall scenario.

Most imports from China will likely remain costly, prompting American firms to continue exploring overseas alternatives, leading to a more intricate supply chain. It is clear that, regardless of the outcome, the effects will be significant. Anticipate observing indications of that in the comprehensive data schedule for this week.

However, proceed with caution! The situation also indicates numerous chances to identify a downturn where none exists.

Consider the manufacturing sector. The upcoming ISM survey will highlight the precarious circumstances currently facing the sector. The situation has not appeared favorable since the immediate aftermath of Covid.

At that time, as the manufacturing surveys began to decline, discussions surrounding a potential recession escalated quickly. Despite various challenges, the economy continued to demonstrate resilience. Such behavior serves as a reminder that manufacturing is no longer the leading economic driver in the US, as it once was.

The comparison to the pandemic appears especially relevant now, considering the discussions surrounding empty shelves and supply chain disruptions. However, it isn't an ideal comparison. The economy was driven by pandemic stimulus measures and the resulting demand for services, both of which have now faded.

Given the decline in savings and confidence and increased delinquencies, the consumer is currently in a weaker position to manage the financial impact of supply chain disruptions.

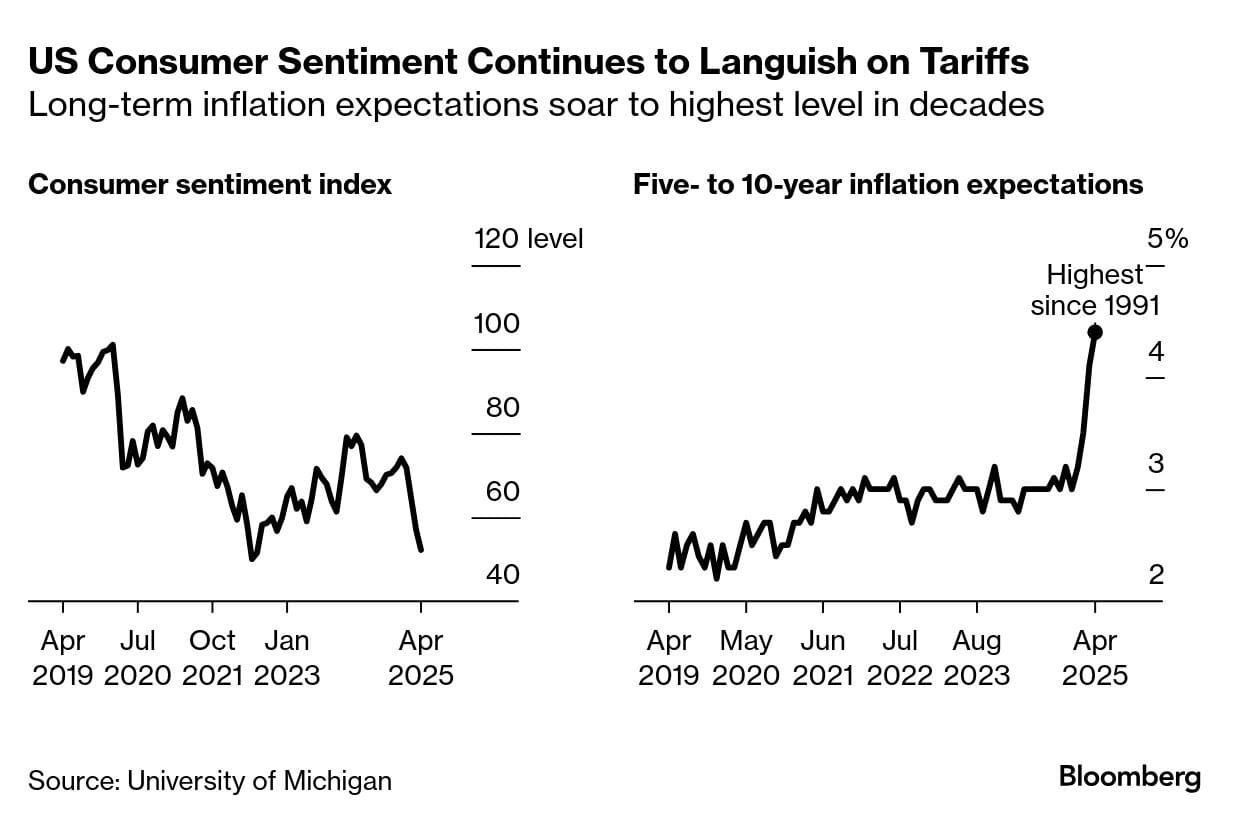

On the economic front, Trump's constituents are unprecedentedly concerned. The latest data indicates a significant decline in consumer sentiment in the US, reaching one of the lowest levels recorded. Additionally, long-term inflation expectations have surged to their highest point since 1991, driven by concerns regarding the domestic impacts of the tariffs implemented.

Realistically speaking, much of this has been the case for some time, and experience has shown us that underestimating the US consumer can lead to significant consequences. Recent years have demonstrated that households exhibit reduced sensitivity to elevated rates compared to previous times. But experts view Trump's policies, especially his global trade war, as creating an uncertain likelihood of a self-induced recession.

A recent ABC-Ipsos poll indicates that 70% of Americans believe the Republican's tariff strategy will lead to increased inflation, which was the primary focus of his campaign in the previous presidential election.

A recent average of polls from the New York Times indicates that Trump's overall approval rating has consistently declined since he assumed office, currently standing at 45%.

A significant portion of those surveyed in a New York Times/Siena poll indicated their discontent with Trump's attempts to consolidate authority within the executive branch.

Last Friday, market observations indicated that the dollar index marked its most significant decline in the initial 100 days of a US presidency, based on historical data dating back to the Nixon administration's departure from the gold standard.

However, Treasuries experienced a rally as investors focused on indications that the US-China trade tensions might be easing.

There were also some positive developments in the equity sector.

For cryptos, the narrative looked positive this week.

This week presents a fundamental issue to address, primarily due to the effects of front-loading on the data.

The impact of households and businesses attempting to preemptively navigate tariffs has been felt across the entire spectrum, from imports to retail. Imports received the brunt of that.

If GDP, manufacturing, and loan delinquencies are not dependable indicators of a recession currently, what alternatives should we consider? The likely response pertains to the employment landscape. Shifts in unemployment frequently mark the beginning and conclusion of recessions.

Even in this context, there remains potential for misunderstanding. There was a notable increase in layoff announcements in March, particularly within the government sector.

We will likely observe additional insights in this week's April data from Challenger. However, it resembles the earlier discussion on manufacturing—is the situation in the public sector entirely disconnected from the private sector?

It is a possibility. The jobless claims data, excluding government figures, do not indicate any significant concerns. It may be an irrelevant consideration if the tariffs begin to exert significant pressure on employment in other areas.

A definitive indicator of a recession is the emergence of negative payroll figures. We are not in that position; however, analysts anticipate that the job numbers will be less robust next week.

If these indicators continue to show weakness as we approach summer, it is probable that the data will serve as the impetus for the Federal Reserve to initiate rate cuts again.

The increase in unemployment ultimately led to a 50 basis-point rate reduction last September. That could resonate positively with equity markets. Last year, the increase in unemployment we observed during the summer was misinterpreted.

The hiring figures serve as a lagging indicator, and a significant downturn in these numbers poses a tangible risk of the Federal Reserve becoming out of sync with the economic landscape.

Elsewhere

Blockcast

How Startale Group is Building "Web3 for Billions of Users"

Ever wondered how Web3 will reach billions? Tune in as we chat with Sota Watanabe, CEO of Startale Group about his ambitious vision. Startale's portfolio includes Astar Network and the exciting new Ethereum Layer-2, Soneium, developed in partnership with Sony Group using Optimism's OP Stack for faster and cheaper transactions.

We unpack Soneium, their new cost-effective Ethereum Layer-2, the groundbreaking collaboration with Sony, and Sota's insights on the future of blockchain. Get ready for a deep dive into the next evolution of the internet!

Blockcast is hosted by Head of APAC at Ledger, Takatoshi Shibayama. Previous episodes of Blockcast can be found here, with guests like Jacob Phillips (Lombard), Chris Yu (SignalPlus), Kathy Zhu (Mezo), Jess Zeng (Mantle), Samar Sen (Talos), Jason Choi (Tangent), Lasanka Perera (Independent Reserve), Mark Rydon (Aethir), Luca Prosperi (M^0), Charles Hoskinson (Cardano), and Yat Siu (Animoca Brands) on our most recent shows.

Consensus 2025, Toronto

We're a media partner for Consensus 2025, held in Toronto, Canada on 14-16 May. Coinbase, BlackRock, Google & The White House Will Be There – Will You? Use the code BLOCKHEAD20 for 20% off tickets!

{kind=link}