Table of Contents

Despite August's smaller-than-expected employment gain, the US jobs report contained enough information to leave markets guessing whether the Federal Reserve would lower interest rates by 25 or 50 basis points (bps) on September 18.

BRN still expects the Fed to pursue a 25 bps increase, but it's a tight call since lead signs indicate additional deterioration is on the horizon.

50 bps or 25 bps? That is still up for grabs.

"We expect inflation worries to subside and the Fed to seek to head off labour market deterioration, which will become more obvious in the coming months. Therefore, we have a 25 bps projection, but it's a low conviction call," BRN lead analyst Valentin Fournier said.

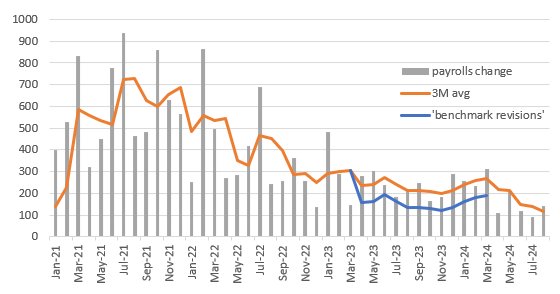

Looking at the August figures, headline non-farm payrolls increased by 142,000, which is lower than the consensus estimate of 165,000. However, adjustments to the previous two months showed decreases of 86,000.

After the revision, three-month payroll growth slowed to the lowest since mid-2020.

The data has been revised downwards regularly recently, and that doesn't even account for the changes made to the provisional benchmark a few weeks ago, which revealed that the BLS underestimated payroll increases by an average of 78,000 each month in the twelve months leading up to March 2024.

Blockhead

Blockhead

Consider the following: June's original count was 206,000, which was changed to 179,000 last month and is now at 118k; July's original count was 89,000, which was revised down to 114,000.

Is Friday's figure truly reliable? To compensate for the mistake in the BLS model, is it necessary to subtract 78,000 from the headline figure? That would result in a mere 64,000 increase in payrolls.

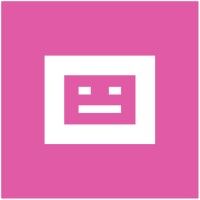

The jobless rate climbed from 4.1% to 4.3% last month and has now fallen back to 4.2%. Despite this, the underemployment rate increased from 7.9% to 7.8%, indicating that more and more individuals are working part-time but would prefer full-time.

According to the data, production appears to be quite lacking in this area (-24,000).

Positions in retail and temporary services have been down for three months in a row, while tech roles have either remained stable or declined for five months.

Government (+24,000), leisure and hospitality (+46,000), and private healthcare and education (+47,000) remain strong points. Jobs in these fields tend to be lower-skilled, less permanent, and more part-time.

BRN contends that the facts are less compelling than what the title implies; the business services, manufacturing, transportation and logistics, technology, and other sectors that one would expect to see in a robust economy are underperforming.

Ashrith Rao

So, are the "good jobs" going away?

There is a clear disparity between full-time and part-time employment. This supports the theory that the United States is gaining mostly lower-paying part-time jobs while losing full-time, well-paying jobs mostly due to attrition rather than replacing employees who resign or retire.

This is how every recession begins. Replacing employees is the quickest method of saving money, but if everyone does it, the economy will stall, and firms will start cutting corners later.

There is no pressing need to act quickly regarding the Fed decision because data indicates that a 25 bps cut is more probable than 50 bps.

However, the employment market is notoriously slow to change in economic cycles, and this one is certainly cooling down.

After Fed chair Jerome Powell warned that "we don't seek or welcome further cooling in labour market conditions," there's good reason to choose 50 bps now rather than wait for any downturn.

Though he will propose it, he may face resistance from certain regional presidents.

BRN suspects this won't be a unanimous choice, unlike in the past.

Following this, we get CPI, which, if core inflation surprises with a 0.3% month-over-month increase, may utterly debunk the 50 bps cut theory.

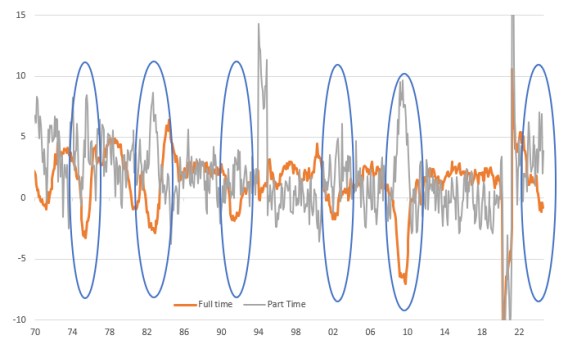

Asset Performance During Fed Easing Cycles

Gareth Nicholson, chief investment officer (CIO) and head of managed investments for Nomura International Wealth Management, said: "History doesn't repeat, but ..."

Nomura's chart below shows the performance of asset classes based on aggregate returns of indices during previous Fed rate cut cycles (2001-20). Alternatives, led by gold, have been the top performers, while equities have fared the worst.

Blockhead

Blockhead