Table of Contents

Before the Federal Reserve's upcoming monetary policy announcement on Wednesday, Asian stocks and bonds both surged, echoing trading on Wall Street, which saw US shares hit new highs.

A rebound in US tech stocks supported the rally on Wall Street, with Nvidia leading the pack overnight.

Blockhead

Blockhead

The Fed will likely keep interest rates unchanged for the fifth consecutive meeting. However, attention will turn to the central bank's projections in the dot plot.

The summary of economic projections will reveal valuable insights into whether the robust data is causing officials to reassess their stance on rate cuts or if they remain steadfast in their original outlook of three rate cuts for this year.

Everyone is interested in the pace of the rate cut path, especially stock traders, who will now need that boost for the markets to continue their bull run.

The Fed will engage in detailed conversations about its balance sheet this week, exploring options for reducing the rate at which excess cash is removed from the financial system.

That will be an interesting pivot debate among traders and institutional investors.

Long-term investors are disillusioned by the markets' run-up to repeated record highs this year, with just a pivot from the Fed away from aggressive monetary policy as the base for that play.

"The real question is, will the markets play out a Deja Vu moment again post the Fed? In the run-up to Fed meetings this year, markets have primed to the top and retreated ever so slightly post a 'hawkish Fed.' Despite there being no change in the Fed's tone or language, buy the dips sentiment has played out," said a chief investment officer at a large US asset management firm in New York.

"The big tech stocks show no sign of weariness in the face of AI-craze, barring a few hiccups this year. So, is the Fed news just a ruse in an otherwise disorderly and disconnected stock markets?" added the CIO.

According to the latest BofA fund manager survey, institutional investors are divided about the potential bubble in artificial intelligence stocks.

About 40% believe there is a bubble, while 45% disagree.

Citigroup strategists noted that bullish bets on US benchmark indices have decreased slightly. However, they also report a moderate increase in net long positions, with the risk tilted more towards the upside.

A separate survey conducted by 22V Research revealed that a whopping 56% of investors are convinced that the next move in the S&P 500 will be a "10%" rise.

However, long-term investors are convinced that the current bull rally needs a shoulder to rise further from here.

"The Fed needs to deliver on rate cuts to substantiate the surprising upswing in global stocks this year. The fundamentals at play are well behind the real rise in share prices, whether it is a macro, financial, or corporate profits-based assessment," said a chief financial advisor at a large portfolio management firm in London.

"More importantly, traders seem to forget the economic backdrop may not be conducive for the kind of rally we have seen this year so far," added the advisor.

Blockhead

Bond Traders Blink First & Increase Short Bets

"Don't fight the Fed" is an age-old phrase that still holds for bond traders. They have increased their bets against Treasuries, positioning for the Fed to once again dash hopes of an early rate cut.

According to investment managers, trading data suggests a growing sense of caution regarding the bank's updated forecasts, which may indicate a reduced willingness to implement monetary policy easing.

According to the December forecasts, policymakers had projected three quarter-point cuts in 2024. However, the economy has displayed unexpected resilience, and inflation has remained above the Fed's target.

Investors have faced significant challenges this year due to the rise in bond rates, which has dampened hopes for a substantial easing of Fed policy.

Before the end of the year, futures traders indicated a strong likelihood of the central bank cutting rates at the upcoming Wednesday meeting, with six anticipated rate decreases through the year.

Traders have revised their expectations and are now predicting three rate cuts in 2024, which aligns with the Fed's dot-plot projections from December.

So, will policymakers dial back on the dot plot?

Well, at least that is what bond traders buying derivatives to hedge against a rise in Treasury rates are saying.

If the latest report indicates that policymakers expect even smaller cuts, another wave of sales is on the horizon.

However, there are still indications of bullishness in the Treasury market and widespread speculation that rates would fall later this year.

Analysts predict 2-year Treasury yields to rise to a year-high of 5% and above if the Fed's dot plots show only two rate cuts instead of the three predicted previously.

The derivatives market clearly points to that risk based on current positioning.

On Monday, open interest in two-year note futures increased significantly, in line with the formation of new short positions.

Options tied to the Secured Overnight Financing Rate, which closely follows the course of the central bank's policies, have also been sought by traders as a hedge against a hawkish turn.

Hedging for higher rates has also been going further on the Treasury options curve.

Data from the CFTC showed that around 183,000 10-year note futures were liquidated in the week leading up to March 12, indicating a trend of de-leveraging from Treasury futures and a potential shift towards credit.

This suggests a net-long liquidation by asset managers. Asset managers' net long posture in Treasury futures has reached its lowest point since July, based on the 10-year note futures equivalents.

The rapid unwinding of short Treasury futures bets by hedge funds suggests a decline in basis-trade holdings.

Analysts at Bank of America say asset managers are refocusing their efforts on investment-grade credit, which has led to a change in posture and a decline in the basis trade.

Dollar Wrong-Footing Investors?

The dollar's recent comeback is driven by central banks reportedly planning to lower interest rates in a synchronised fashion.

Wall Street anticipated a dramatic interest rate reduction from the Federal Reserve at the beginning of the year, which led them to believe that most Group-of-10 currencies would increase vs the dollar.

In contrast, the dollar has surpassed most of its major competitors this quarter, with a notable gain of more than 2%.

The reality that the US is not acting alone and a change in expectations about the size of Fed cuts are reflected in the dollar's performance.

A study of economist predictions and BIS data indicates that the Fed is expected to be one of ten major central banks to cut interest rates in the second half of this year.

This synchronised policy loosening cycle is the most noteworthy in sixteen years, reflecting the worldwide economic downturn.

Notable among these institutions is the Bank of Japan, which has broken tradition by ending its aggressive monetary stimulus plan and eradicating the world's last negative interest rate.

Past data shows that when most central banks eased policy simultaneously, the dollar gained almost 3% every quarter on average.

The greenback is expected to keep its edge due to the Fed's policy rate, which is expected to be among the highest among major developed countries by the end of this year, second only to New Zealand.

With investors adjusting their expectations for policy easing and the global economy showing resilience against a recession, the dollar may gain strength, which may seem paradoxical.

The dollar benefits from various factors, such as a yield premium and a robust US stock market attracting capital investments.

It remains to be seen whether the Fed will disrupt that trade flow and make traders' wagers 'gloriously wrong'.

Yen Down Despite BoJ's First Hike Since 2007

Speculation that the Bank of Japan will maintain its accommodating monetary policy after ending the world's last negative-interest-rate programme on Tuesday caused the yen to fall versus the euro to its worst level since the financial crisis 2008.

As it continues its roughly 7% decline this year, the yen is slipping towards a level not seen since 1990, making it the worst performer among G10 currencies.

Many believe that the yen will continue declining due to Japan's lower yield than other developed countries, particularly the US.

Japan recently increased interest rates for the first time since the financial crisis and changed its yield-curve control regime.

However, BOJ Governor Kazuo Ueda and his staff clarified that they expect financial conditions to remain relaxed.

Opinions vary among speculators regarding the timing of the central bank's next interest rate hike.

So, the yen's break lower is a common betting theme for the moment.

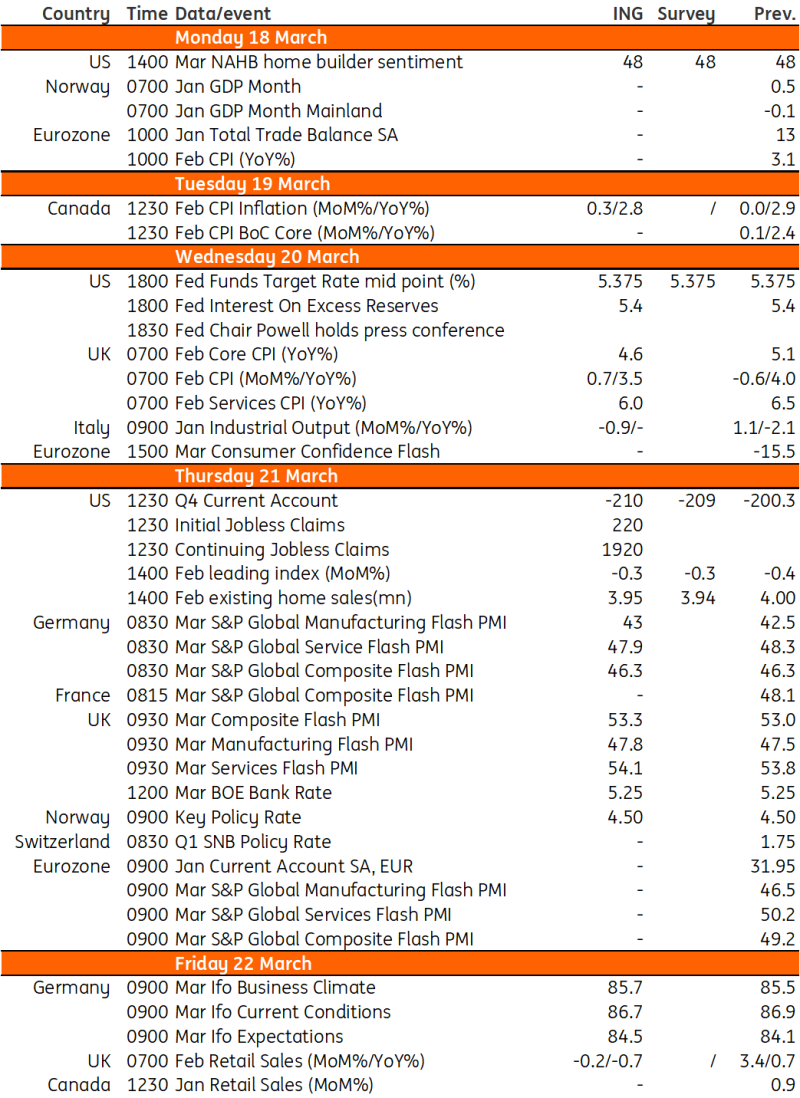

THIS WEEK

The Federal Reserve's policy meeting takes centre stage this week. Following a series of hot data releases, the next move as a cut in June is dividing analysts and traders.

In the UK, all eyes will be on the release of inflation data, before the Bank of England meeting on Thursday. In market view, the first UK rate cut will come in August.

Macro Data Calendar

What to Watch on the Fed?

The projections of FOMC members will be the centre of attention. In their December forecast update, the Fed indicated that they believed three 25 basis points (bps) rate cuts would be the most probable trajectory for 2024, with an additional 100 bps of cuts anticipated for 2025. Markets anticipate a comparable set of projections at the 20 March FOMC meeting, with the messaging suggesting that the Fed is leaning towards reducing rates later this year.

However, they require further evidence to substantiate this course of action. Considering the varying predictions from individual Fed members, a slight shift in the projections of just two out of six FOMC members could alter the median dot, indicating either two or four rate cuts in 2024 instead of the current projection of three.

The possibility of a reduction to two rate cuts instead of three carries a greater level of risk compared to the Federal Reserve indicating four cuts.

The Fed aims to prevent a recession if possible. Markets anticipate that they will be able to transition their monetary policy from a restrictive position to a more neutral stance before the summer.

According to current suggestions, the neutral Fed funds rate is estimated to be around 2.5%. This implies that there is potential for up to 300 basis points of cuts to reach a "neutral" level.

Markets believe they may not be inclined to go to such an extreme extent considering the likelihood of continued lenient fiscal policy regardless of the outcome of the November presidential election.

However, analysts currently anticipate a reduction of 125 basis points this year, commencing in June, followed by an additional 100 basis points in 2025 as optimism grows for a smooth economic transition.

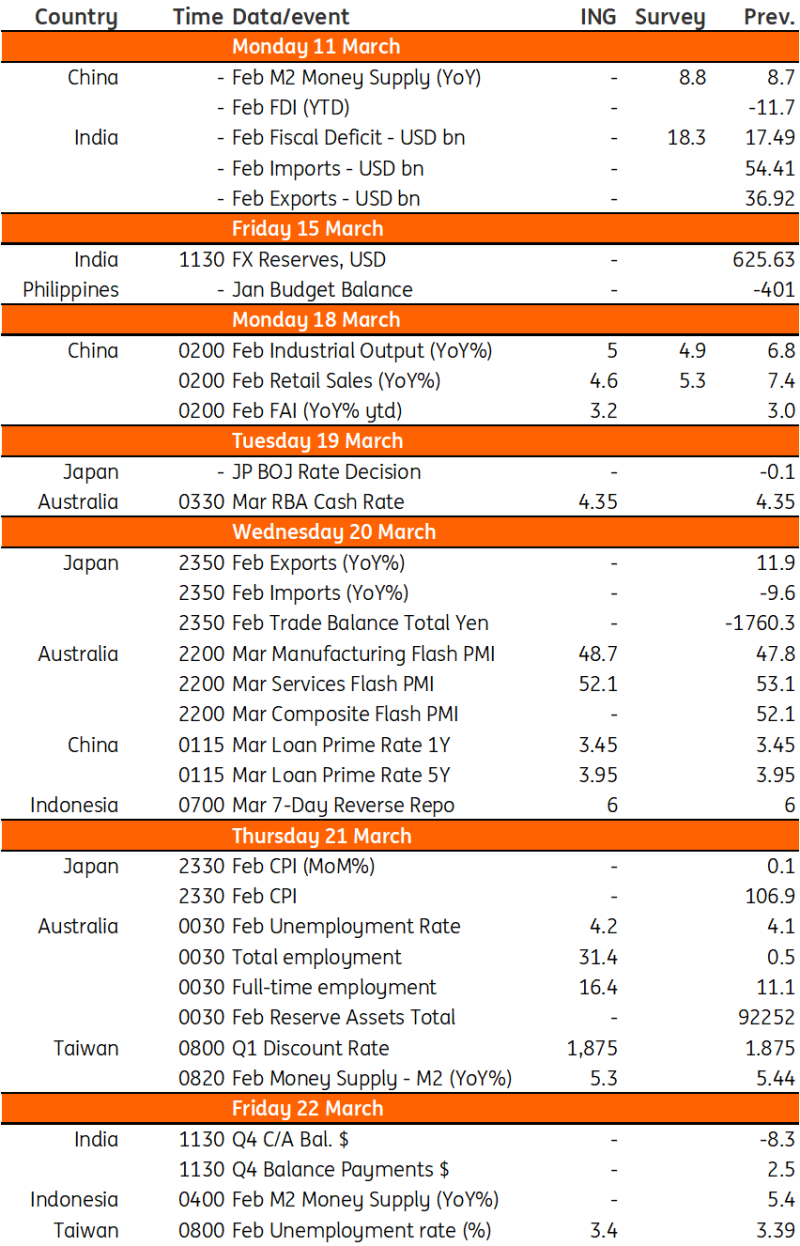

This Week in Asia

A first look at China's 2024 hard data after the Two Sessions shows a small uptick in an otherwise listless economy. The unemployment data will also be published, with the surveyed jobless rate expected to stay stable at 5.1%.

Macro Data Calendar

Is AI-Hype Hurting Emerging Markets?

Developing countries' capital markets are being drained by the unstoppable surge in US-led AI stocks, with the so-called 'magnificent seven' savouring the flow.

Investors worldwide have been drawn to the impressive accomplishments and bright prospects of US companies, including chipmaker Nvidia.

This year, the S&P 500 Index has soared to unprecedented levels, driven by the remarkable performance of seven prominent companies: Nvidia, Apple, Microsoft, Amazon.com, Meta Platforms, Alphabet, and Tesla.

Due to the current AI frenzy, stocks in developing markets are currently trading at the cheapest and an unprecedented level when compared to the S&P 500.

Over the past three years, the MSCI ACWI Index has experienced a 15% gain, while emerging market equities have unfortunately seen a decline of 23%.

Until there is clarity on the Fed's rate cut path, a boost to emerging markets remains elusive even as bets in favour of big US tech-driven by AI are the order of the day.

Southeast Asia Blockchain Week to Kick Off in Bangkok

Blockhead

Southeast Asia Blockchain Week (SEABW)'s main conference will take place at the True Icon Hall from 24-25 April, and Blockhead will be there as a media partner.

The main conference will be held over two days (24-25 April) at the True Icon Hall. Guest speakers include Arak Sutivong, Deputy CEO at SCBX, Yoann Turpin, Co-Founder at Wintermute, and Kelvin Koh, Co-Founder and Managing Partner at The Spartan Group.

Demo Day, which will take place during the main conference, will showcase the hottest projects in the region and provide the opportunity to connect with early-stage startups. Game Day will put the spotlight on the blockchain gaming space, featuring tournaments and interactive activities.

Blockhead

Blockhead Blockhead

Blockhead Blockhead

Blockhead Blockhead

Blockhead

{kind=link}