Table of Contents

We previously talked about how some aspects of the Celsius saga are similar to, but likely to end worse for investors than, the famous Madoff Ponzi scheme. With the latest Celsius filings, this is clearer than ever.

Revealing transactions

There has been a lot of uproar over Celsius’ bankruptcy filings semi-doxxing many of their creditors. As Celsius was not any sort of regulated financial institution, the creditors had no reasonable expectation of privacy during insolvency proceedings. The ruling is a relatively easy read and is filled with these sorts of passages that make it clear the patience required to be a judge:

Not to break any news here but the whole “Do UK laws take precedence over those passed by the US Congress?” thing was settled quite a long time ago.

Beyond spurious legal arguments, these same filings say a lot about the dealings of Celsius management. And quite a lot of what is contained in these filings looks truly egregious. There is no question that of all the insiders only a handful received the vast majority of the extracted value. And the big headline out of these filings concerns large withdrawals from the most senior insiders near the end.

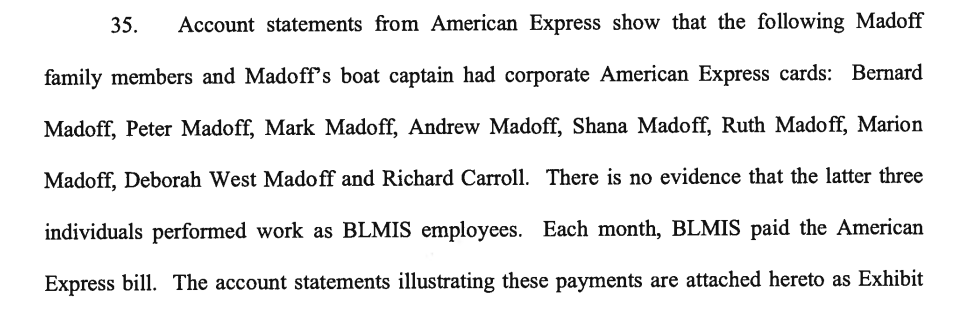

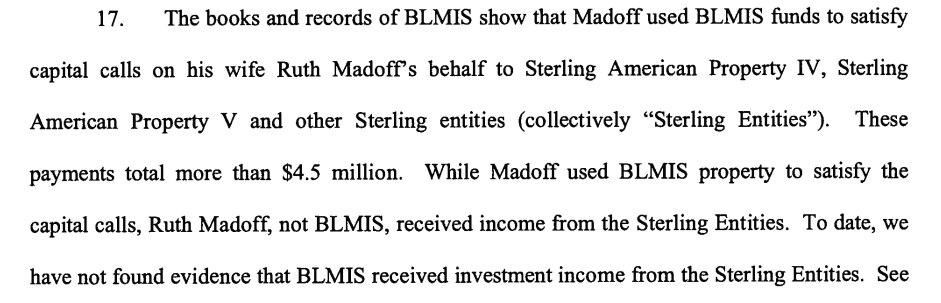

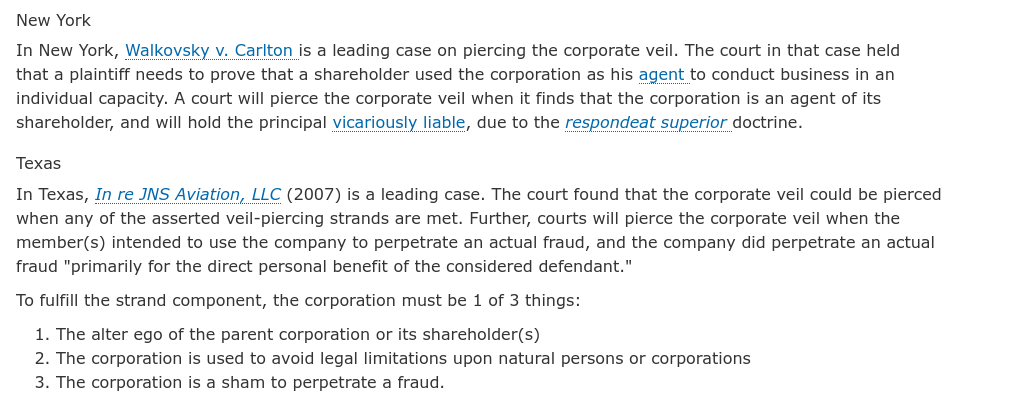

If, and it’s a big if, creditors can establish a pattern of behaviour they can “pierce the veil” and go after those people’s personal assets. In the Madoff case the creditors got access to nearly all of the Madoff family’s assets. The relevant filing there is this one which details how the business and personal affairs of the family were incredibly intertwined. Just one excerpt beautifully illustrates how the Ponzi scheme and family finances were one and the same:

If your boat captain has a corporate card, it’s going to be hard to argue your personal assets are separate from the business. That document also contains stories of arbitrary payments, loans to related parties and the financing of various not-business-related-at-all ventures undertaken by family members.

Celsius management shows some of the same features.

Random bonuses

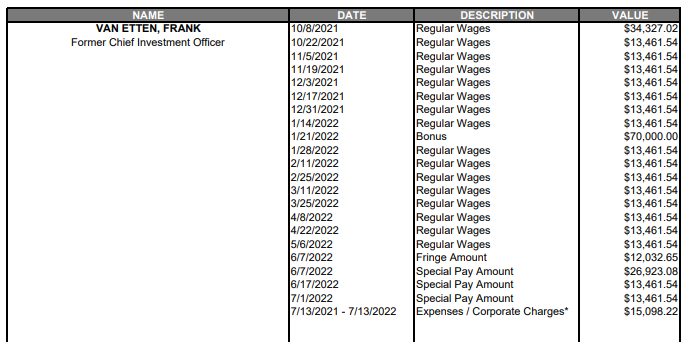

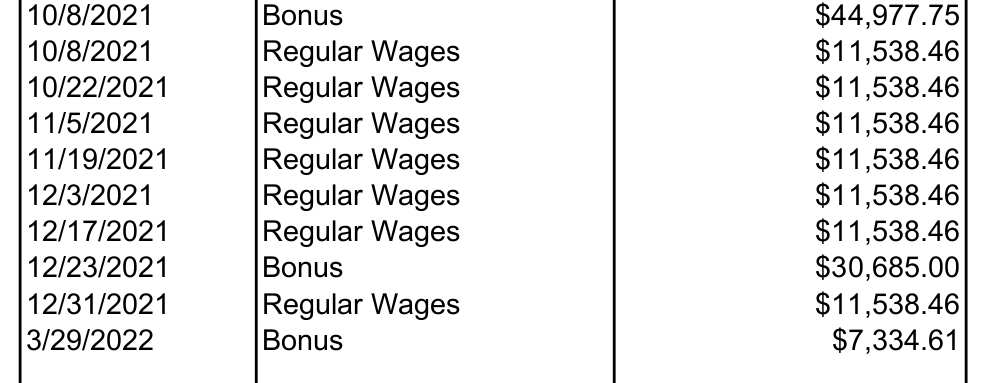

First up, their former CIO collected a “fringe amount” of approximately one paycheck, and then four more paychecks worth of cash listed as “Special Pay Amounts” just before bankruptcy. No other employee in the filings has these sorts of payments (and the word fringe appears nowhere else). Note they paused withdrawals on the 13th of June – so these payments began before the pause and continued after it. This certainly looks a bit like a cash handout to a favoured party.

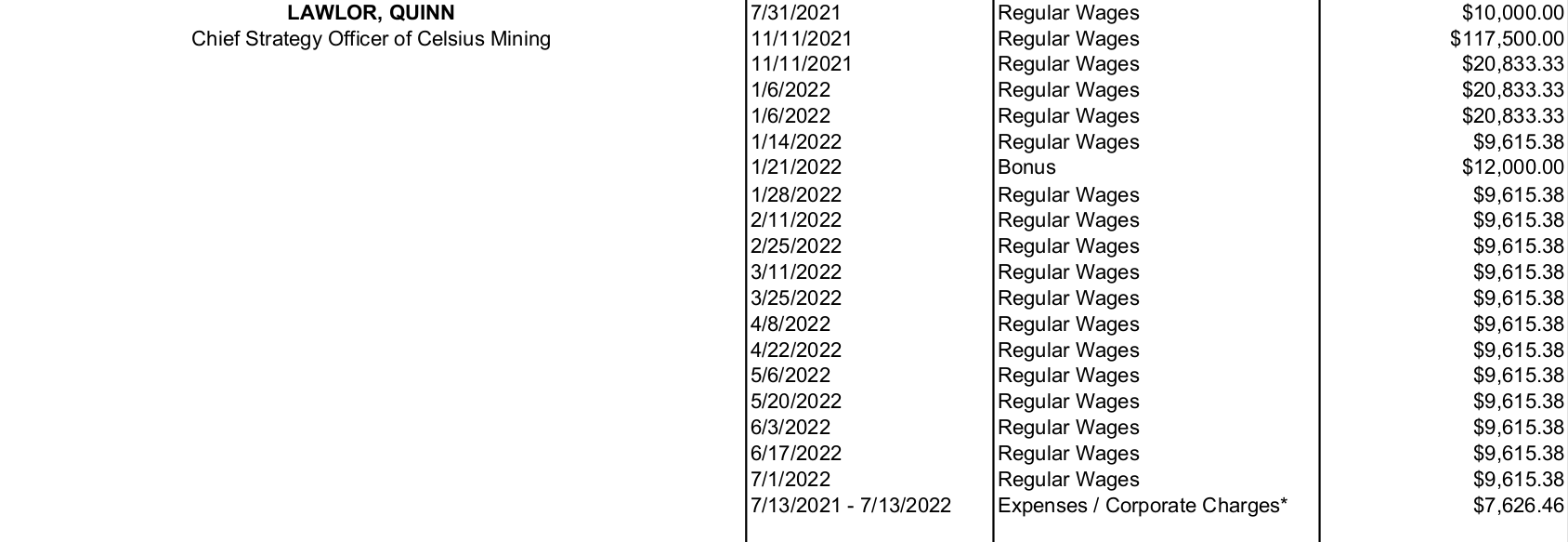

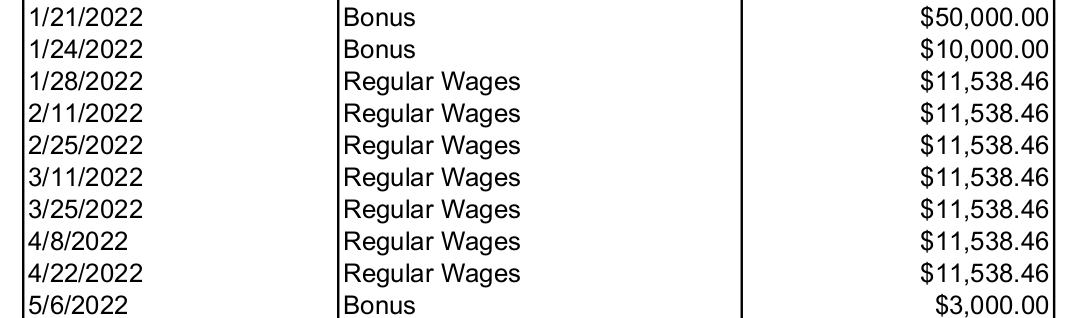

We can also find completely ridiculous payments:

Calling that sequence “regular wages” does not qualify as English. And even without reviewing a single other document we can all agree there is zero chance that stream of paychecks was consistent with a written contract.

And there is more!

That’s the chief strategy officer taking a US$ 4 million loan out in April. It was collateralized by CEL:

There looks to have been another loan in May, though only the deposit and collateral are disclosed:

A few other folks look to have taken smaller loans, including against other tokens. The Madoff case also involved odd loans, though more-directly personal perhaps than these and certainly larger.

We also find a smattering of irregular bonus payments to other members of the management team:

Those are but four examples. The issue is not so much the amounts as the randomness. Who gets paid a bonus three times within six months? And these are not employees collecting commission. Those snippets include the global head of business process and general counsel. At a minimum, this company did not have standard processes and controls. And, truthfully, one might question how much of a “real company” it was at all.

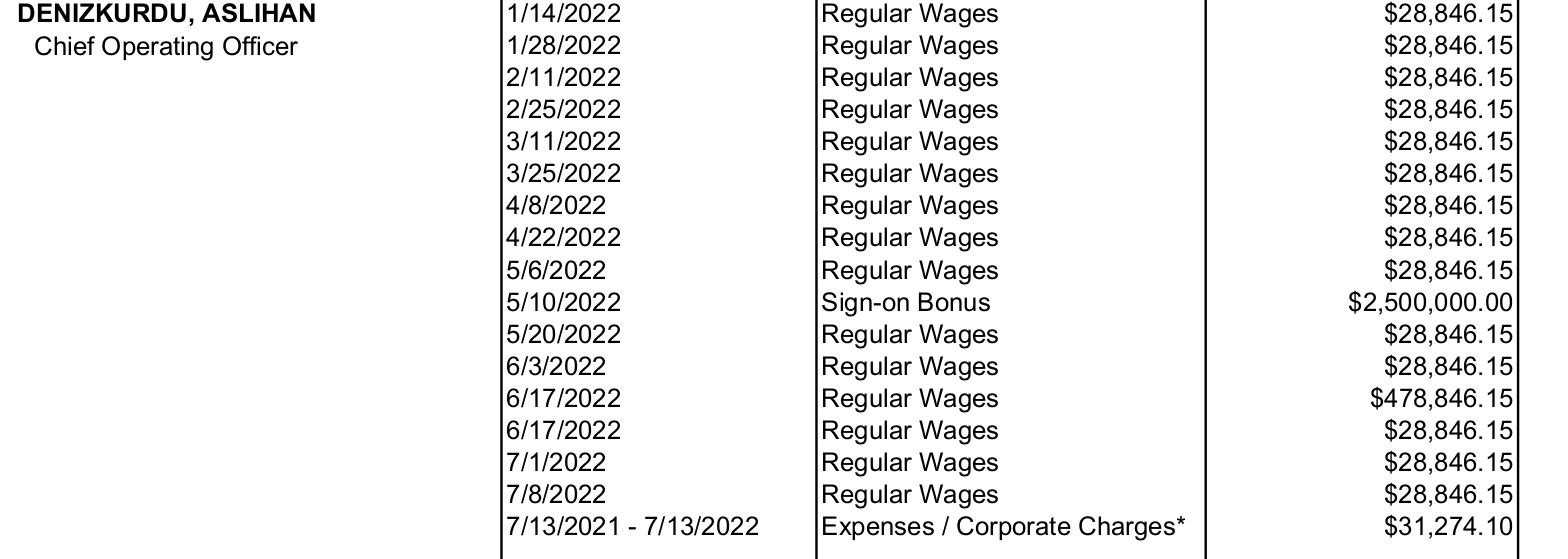

The one person who looks smart in all of this is their COO. She was hired in January 2022 from Citibank and received a large cash sign-on bonus.

Now this executive was a long-time banker and one imagines that was simply buying them out of deferred stock or so. The date, the Tuesday after the LUNA weekend, is worth noting. Surely we will learn more there.

CEL team wallet sale

Perhaps most galling for CEL token holders are the many lines labelled “CEL Team Token Sale”

That number is in Israeli Shekels (ILS). The total in ILS is about US$400,000 worth. Not huge but given what has happened with the token its quite the coup-de-grace that team members were organizing selling and collecting the proceeds alongside their Celsius paychecks! There can now be no question that the CEL team within Celsius was trying to extract value for themselves from the token and using corporate resources to do so.

Also note that the team was managing assets for their own benefit within the company’s accounts. We would need more documentation to understand the whole story for sure but this certainly looks like a mixing of personal and business assets.

It is also worth mentioning that the “but this is how hedge funds work” argument cannot apply here because, yeah, nothing was registered as such or participated in any of the regulatory disclosures that would have then been required. When your best defense is that critics misunderstand the type of fraud you are perpetuating things are not looking good.

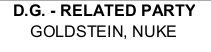

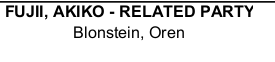

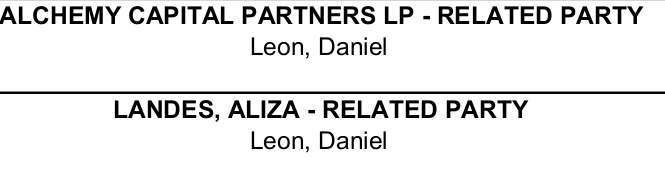

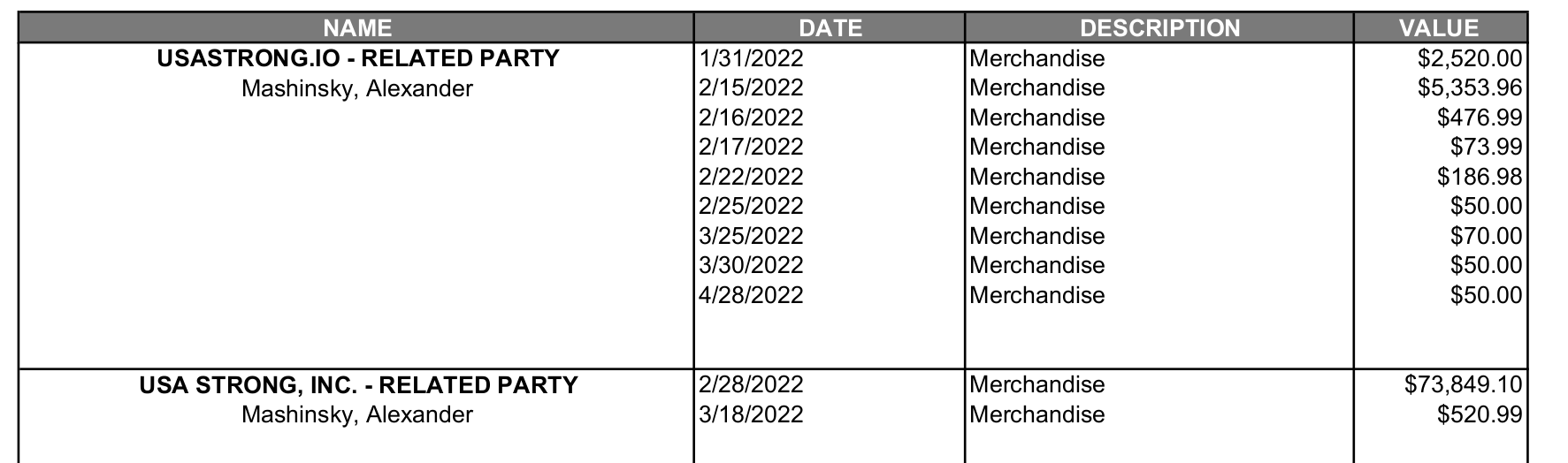

A festival of related parties

There are so many related parties here — both legal entities and presumably family members — that it boggles the mind. There is a series of Mashinsky entities named Koala 1, Koala 2 and Koala 3 which is not terribly creative. Nuke Goldstein had a “Bits of Sunshine LLC” which is a bit more like it.

A lot of dealing with related parties, or a lot of hiring of relatives by senior management, are both bad looks. But here the Chief Compliance Officer looks to have hired a relative and at least half a dozen people or entities related to the CEO were actively doing business with Celsius. Now read this passage from the Madoff document:

And compare to the Celsius docs:

Is there a real difference here beyond the amount of money?

And?

None of this amounts to conclusive evidence any sort of crimes were committed or otherwise out-of-bounds behaviour occurred. But the creditors can — and probably will — have a go at accessing the personal assets of at least some management and their families. To quote the Cornell Law School primer linked above:

After looking at the excerpts above reasonable people may disagree on whether these sorts of conditions apply. And nobody expects that more junior employees, or members of the CEL team, will be subject to wholesale seizures.

But clawback attempts are pretty clearly coming for some of these folks. Money the CEO took out or transferred to related parties will be easy to retrieve. But the habitual random bonuses handed to executives? That money is probably gone. And who knows what happens to interest paid out on deposits from companies related to co-founders.

This confusion in and of itself is worse for the creditors than a plain-old Ponzi scheme. The Madoff insiders really had no defense to the claims on their personal assets. The management team here can, and surely will, try. Plus the expenses keep running and an awful lot of cash that escaped Celsius’ corporate coffers is looks unlikely to come back.

Related: Worse Than a Ponzi Scheme

{kind=link}