Table of Contents

This column explores cryptocurrency markets from the perspective of a somewhat-grizzled trading veteran with a quantitative background and perhaps too much experience doing derivatives janitorial work. Finance is an old industry with a long history of everything from productive innovation to cartoonish fraud. Here we take a grand skeptical tour of a new corner of that world, with two tools that have consistently helped traders for millennia in our steamer trunk: math and knowledge of the past.

This past week we got a look inside two alternative financial institutions when Euro Pacific Bank was shut down and Celsius got sued by a former employee/partner/contractor. These are still ongoing matters – Euro Pacific’s management is trying to salvage the situation, and Celsius remains frozen – so it is hard to know things for certain. But for now let’s take the concrete, evidence-supported claims in those documents at face value and see what we can learn.

These two institutions were trying to remake banking in different ways. Celsius tried to cut out costs so they could pay investors higher yields. And Euro Pacific was all about zero leverage and maximum safety in banking.

These do not, at first, sound like similar goals. And these two organizations are run by very different people. Their debate last year on Kitco was wonderful and everyone should watch it.

Those differences aside, it looks like both operations were predicated on the same two mistaken assumptions about traditional finance: that it is incredibly inefficient and that fractional reserve banks are always teetering on the edge of insolvency.

Efficiency

First let’s look at these efficiency claims. Celsius was flogging 8%+ deposit rates on USD stablecoins at a time US T-Bills paid under 1%. Alex Mashinsky, Celsius’ founder and CEO, claimed this was possible because the traditional financial system was robbing people and somehow competition is so poor this inefficiency never disappears. If that was true they could simply loan funds out for high yields, have a low cost footprint, and ride off into the sunset. This does not fit with the conduct alleged in the KeyFi lawsuit:

Prior to Plaintiff coming on board, Defendants had no unified, organized, or overarching investment strategy other than lending out the consumer deposits they received. Instead, they were desperately seeking a potential investment that could earn them more than they owed to their depositors.KeyFi vs. Celsius, paragraph 3

Now that statement may be self-serving on KeyFi’s part. They are, after all, suing Celsius so it’s unsurprising they’d impugn their competence. But we do know, empirically, that Celsius ran out of funds and paused withdrawals.

Read more: Below 0° Celsius: When Your Deposit Gets Frozen

So at least some part of that last sentence must be accurate. Celsius was promising 5% to 10%+ additional return on assets compared to banks and, empirically, they couldn’t just make that up with better efficiencies. Traditional finance just isn’t that inefficient. Whether there was meaningful theft involved, it seems a pretty safe bet we are going to see investigated in front of a jury.

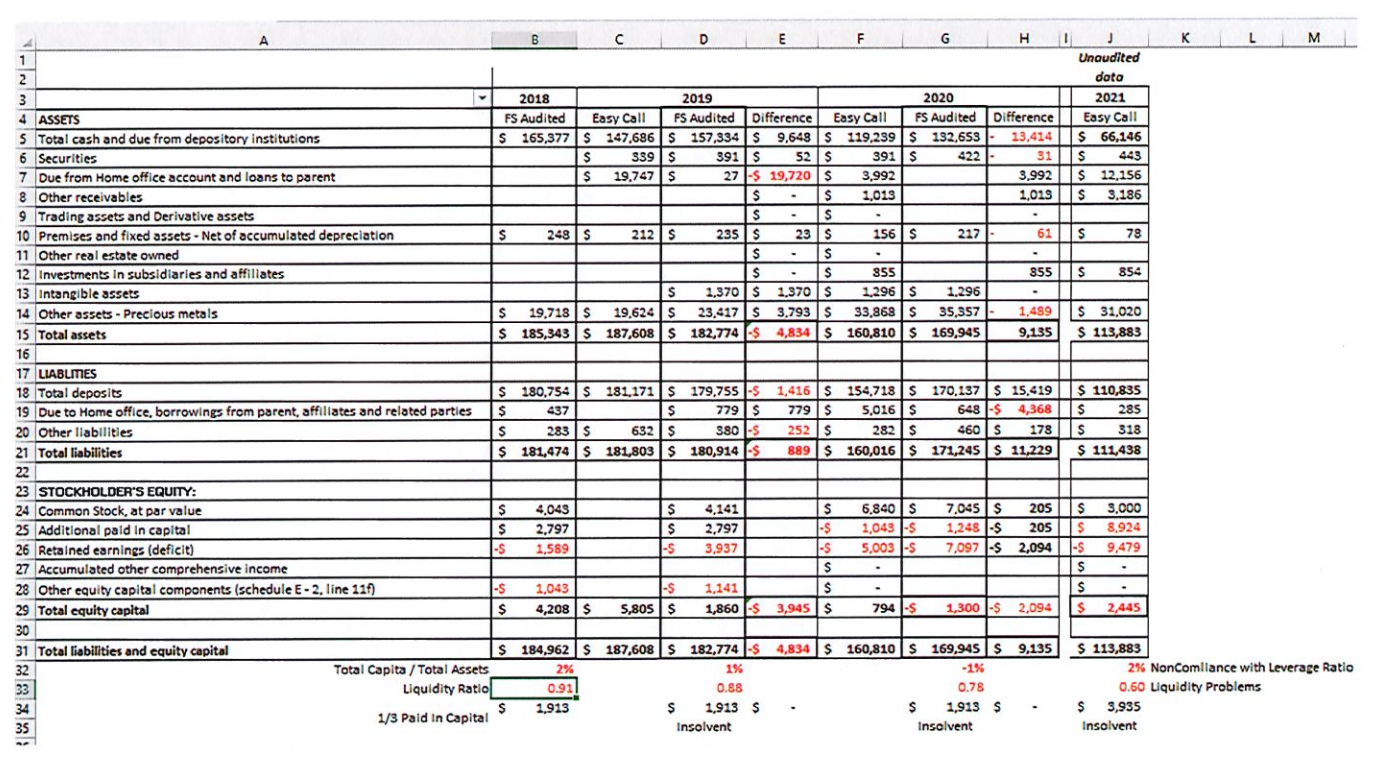

Euro Pacific looks to have had a similar problem. They don’t make loans per their own website. That cuts out some costs for sure! But they were still losing money every year. How do we know? The regulator included a balance sheet snapshot for the bank in their order:

Row 26 shows “Retained Earnings” and we can see it getting more and more negative every year. Whatever was happening at Euro Pacific bank, we know it was losing money. The business thesis, per its own slide deck, was that people would pay fees in exchange for increased safety. Empirically this was a loss-making business plan.

Why does this matter? Bank losses come out of bank capital. And bank capital is the buffer that protects depositors from losses. Normally we worry about a bank making losses on investments. But, from a depositor’s perspective, operational losses are just as bad. Money is fungible after all.

Euro Pacific bank didn’t go out and leverage deposits into bad loans and lose money the way Celsius looks to have done. But losses are losses and it turns out there just wasn’t enough inefficiency to squeeze out to make these alternative business models work.

Fractional reserve

Both these businesses also railed against “fractional reserve banking” as some sort of fraud-adjacent evil. But if we look at how they were organized, this betrays some element of confusion about how banking works. This looks to be the second mistake.

Lots of crypto people think a bank being “fractionally reserved” means it can only honor some fraction of withdrawals at once. Say a bank has 10% reserves; they think this means the bank can only allow 10% of depositors to withdraw their money. The bank has some small pool of cash and is constantly operating on the edge, sneakily trying to avoid blowing up if too many people ask to withdraw at once.

But this isn’t correct at all.

It means the bank can service that amount of withdrawals without selling any assets and without touching its capital. At the same bank if 15% of people try to withdraw the bank will need to sell, or borrow against, some assets. But these assets are normally incredibly liquid government bonds and the like. Bundles of loans are also easy to trade these days. Go look at, for example, Bank of America’s latest financials. It can cover all demand deposits – all of them! – with highly liquid securities. Plus it has a capital buffer of about 8% of assets, meaning for every US$100 it owes to depositors, it has has an extra US$8 owed to nobody as a safety buffer.

Euro Pacific and Celsius look like they were operated by people who believed the mistaken first description was how banks worked. In 2021, Euro Pacific bank lost about US$4 million. And at the end of the year it was holding about US$2.5 million in capital. It lost a few million dollars in every year we can see, all the while holding only a few million dollars in capital, raising equity every so often to stay afloat.

This is not a safe bank! This thing was, truly, always hanging on by a thread.

It does not matter if its assets were incredibly low risk because the bank’s own operations were sufficient to drive it to insolvency. “We have no credit risk but our expenses exceed our revenues” is a weird kind of investment pitch!

Something similar looks to have been true for Celsius as well:

Stone was provided direct access to the 0xb1 account … Celsius and Stone decided to engage in certain DeFi trading activities that required appropriate risk management and hedging to guard against price movements in certain crypto-assets.KeyFi vs Celsius, paragraph 40

We can see action in this 0xb1 account on chain. Whether the allegations are accurate or not it is clear DeFi activities occured, they needed proper risk management, and they didn’t get it. And when losses started to roll in Celsius’ capital was overwhelmed. We know this must be true because it, quite literally, could not service client deposits out of its assets or equity.

These incredible losses meant that the billions of dollars of customer deposits could not be returned to those customers in the event that the customers sought their funds backKeyFi v Celsius, paragraph 9

Even if the KeyFi suit is mainly inaccurate – and we have no real way to judge this now – that sentence is pretty clearly true. Celsius was not able to return assets to their customers! The entire document reads like a description of a business that thinks fractionally-reserved banks are continually insolvent and most of traditional finance is some kind of juggling act to keep this well-known-and-also-somehow-well-hidden insolvency from coming to light. Except that view is completely wrong.

Basic mistakes

Both these operations made the same two basic mistakes. They didn’t keep enough equity on hand to cover losses. And they didn’t keep enough liquidity on hand to service outflows.

Euro Pacific looks to have spent its capital running a loss-making bank while Celsius looks to have simply lost client funds in somewhat-unhinged DeFi trading. Those are not precisely the same things of course. But it really does look like their failed strategies sprang from the same fundamental misconceptions about the way finance is supposed to work.

It will be interesting to see if these two elements pop up again in the deluge of crypto-related litigation we are surely going to see over the next few months and years.

{kind=link}